What the measure is about

The UK has announced a temporary VAT cut from 20% to 5% to ease part of summer costs for families with children. It would apply from 25 June to 1 September 2026, during the school holidays. It is not a general tax cut: it targets children's meals, children's tickets to certain shows and family attractions. Eating out with children, going to the cinema, visiting a zoo or a family theme park should cost a little less that summer, subject to the legal instrument taking effect as HMRC outlines.

Summer as a fiscal battleground

For many families, summer does not start with sunshine: it starts when spending jumps. Children's menus, tickets, day trips, parks, cinemas, museums, transport, activities to fill weeks without school. The British government is targeting that slice of the budget — not the annual tax return, but the small ticket that repeats. The gap between 20% and 5% VAT can look technical, but for a family going out several times in the holidays it becomes a visible signal.

What qualifies for reduced VAT

The reduction covers certain children's meals in restaurants, cafés and similar venues, clearly marketed and sold as meals for children. It also covers children's tickets to cinemas, theatres, concerts, exhibitions and shows sold as child tickets. And admission to certain family attractions, where reduced VAT may apply to all customers when the attraction is suitable for families with children.

Restaurants: you cannot just label any small plate as children's

In catering, what matters is how the product is sold. A dedicated children's menu, priced and presented for children, may qualify for 5%. A smaller adult portion, a discount or a scaled-down main menu is not enough on its own. The business must show clear commercial intent. Takeaway food is not included in this relief.

Children's tickets and family packages

At cinemas, theatres and shows, if adult and child tickets are sold separately, 5% applies to children's tickets. If a family package is sold (e.g. two adults and two children for one price), the whole package may benefit from reduced VAT. Many businesses may redesign family offers so the final price is more attractive without giving up all margin.

Family attractions: the strongest part of the policy

Theme parks, fairs, water parks, circuses, museums, planetariums, zoos, aquariums, farm parks, play centres, trampoline parks and observation wheels may qualify if conditions are met. For these attractions, reduced VAT may apply to admission for any customer, not only children — the whole family visit can be cheaper.

What is excluded: sport, add-ons and out-of-date passes

It does not apply to sport or sporting events. Food, merchandise or upgrades sold separately inside an attraction are not automatically covered. Passes allowing repeat entry outside the relief period may not qualify. Admission may be at 5%; a T-shirt or extra meal may keep normal VAT treatment.

25 June to 1 September: dates matter

The measure applies to supplies where the right of admission or the service falls between 25 June and 1 September 2026 inclusive. Buying during the window is not enough — when the service is enjoyed matters. For businesses with advance tickets or bookings, service date and VAT treatment at till and on invoices are critical.

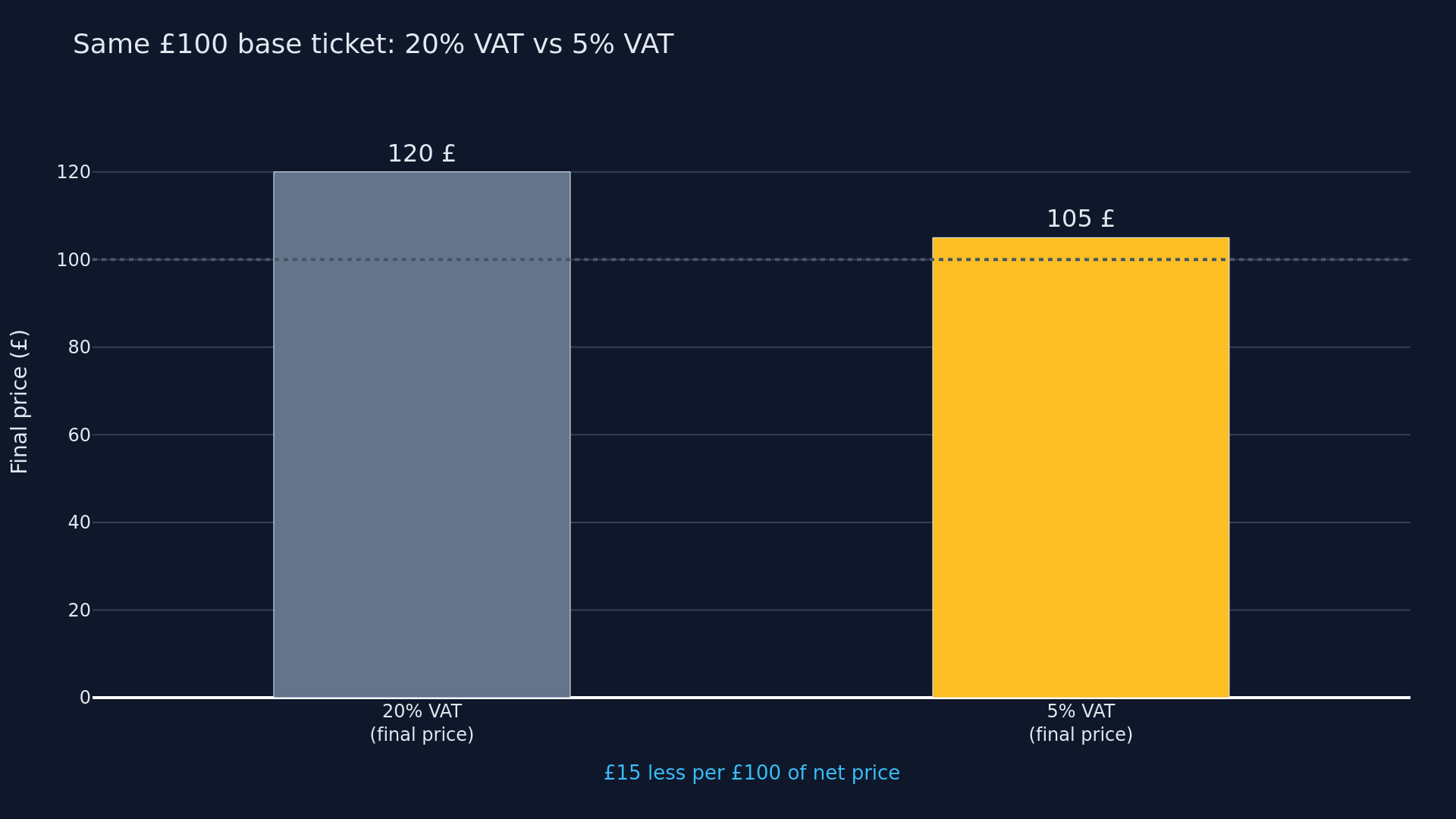

The same ticket at 20% and at 5% VAT

On a net price of £100, the final price falls from £120 (20% VAT) to £105 (5% VAT): £15 less per £100 of net price. A small-looking cut adds up when a family repeats outings all summer.

Visual comparison: 20% VAT vs 5% VAT

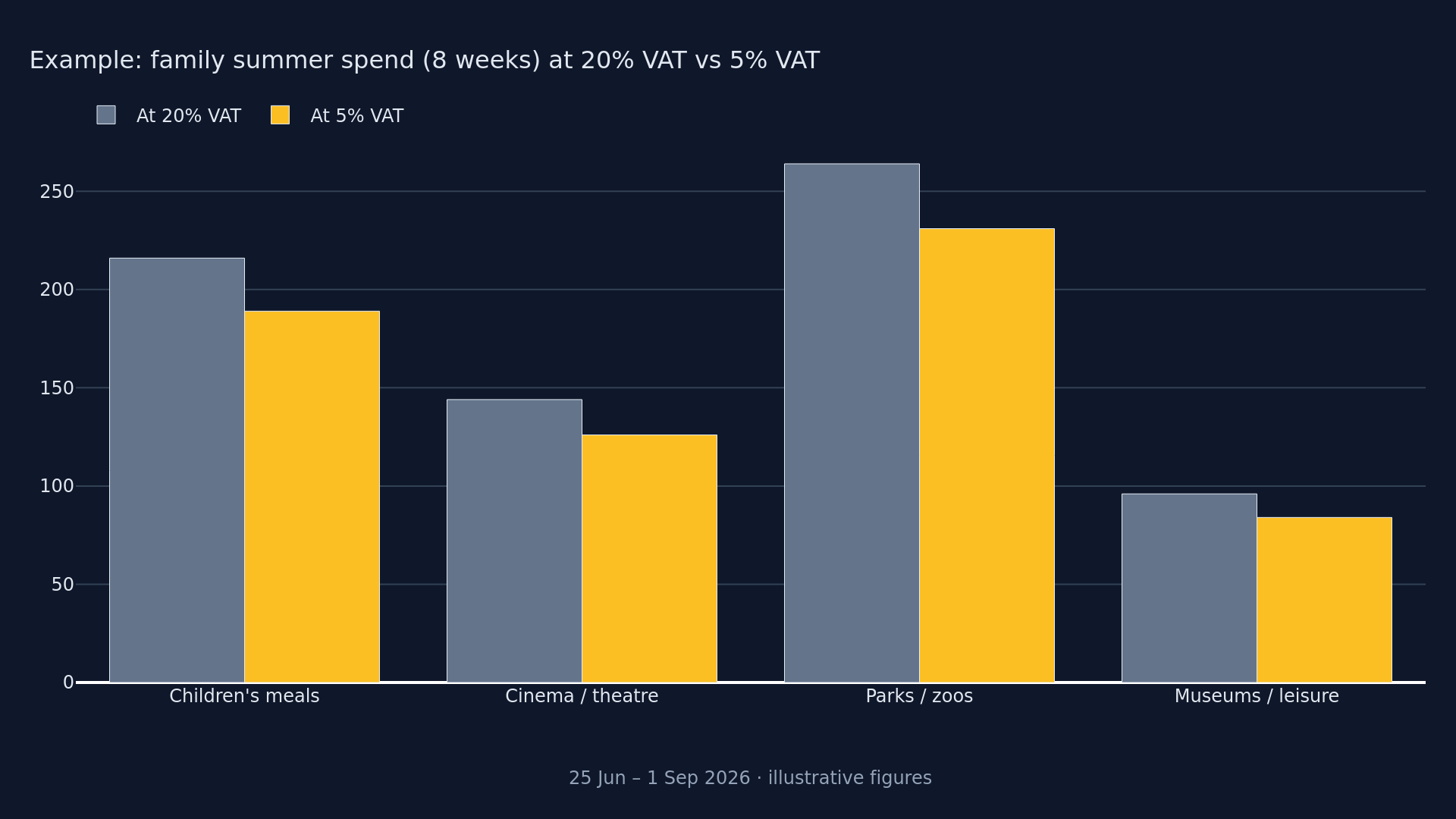

Family summer spending (example)

What it means for families and businesses

For families, the measure may mean a slightly cheaper summer. For businesses, it is a commercial tool — clearer children's menus, family packages, summer campaigns — but also compliance work: menus, tills, ticket categories, bookings and invoicing. 5% does not apply by guesswork; the product must fit HMRC rules.

A temporary cut, not a structural reform

It does not permanently change UK VAT. It is a time-limited intervention for summer 2026, aimed at making certain family spending cheaper during school holidays. Impact will depend on businesses passing part of the relief through to prices and on families responding with more leisure and dining spend.

Conclusion: policy that hits the everyday wallet

The cut to 5% does not change housing or energy bills, but it touches repeated summer spending: a children's meal, cinema, zoo, museum or water park. For a few weeks, on certain family purchases, the UK would take 5% instead of 20%. Guidance: Revenue and Customs Brief 5/2026 (GOV.UK).